Rural women in Papua New Guinea (PNG) face significant barriers to savings and accessing credit. This is due largely to their small and irregular income, household and social demands on their income, high rates of illiteracy and lack of access to the formal financial sector. Women’s limited access to credit and savings mechanisms place barriers on them to take advantage of local economic opportunities to improve household food and income security.

One approach to improving poor rural women’s savings and access to credit in several developing countries has been through the development of informal village-based savings clubs. In 2018 as part of the ACIAR-funded project, “Identifying opportunities and constraints for rural women’s engagement in small-scale agricultural enterprises in Papua New Guinea” a pilot Village Savings and Loans Association (VSLA) scheme was implemented. Researchers from Curtin University and the Coffee Industry Corporation worked in collaboration with CARE International in PNG in two villages in Eastern Highlands Province. CARE International in PNG implemented and managed the VSLA groups. The VSLA model adopted by CARE drew on the VSLA methodology CARE International has used for over twenty-five years in numerous rural communities in Africa, Latin America and Asia.

CARE INTERNATIONAL VSLA MODEL

The CARE VSLA model is based on a small group of up to 25 to 30 members who meet weekly or fortnightly over a nine to twelve month ‘cycle’ to save together and borrow money from the accumulated funds. Prior to the start of the meetings, members attend training over several weeks. The training covers among other topics, the VSLA methodology and financial management.

At the start of a cycle, groups create their own constitution which sets the rules the group will follow (within the parameters of the CARE model) and an elected five-person management committee is formed to administer and manage the savings and loans over the cycle. Savings are through the purchase of ‘shares’, the price of which is determined by group members at the beginning of the cycle. At each meeting members can buy up to a maximum of five shares. When the savings have accumulated, members can borrow money. Loans are repaid with interest and must be repaid within a certain time-frame. At the end of the cycle a ‘share-out’ occurs. At the share-out the accrued loan interest and savings are distributed among individual members, according to the number of shares purchased by each member. Following the share-out, the group may reform and start a new cycle.

In January 2018, two VSLA groups were formed in Nagamufa Village: a women’s group and a mostly male group (with two women). Members of both groups come from four adjoining villages.

NAGAMUFA VILLAGE VSLA GROUPS

None of the women had bank accounts when they joined the group. Members of the VSLA groups are largely subsistence farmers. Men’s primary income source is from the sale of coffee while women principally rely on earning small amounts of money selling fruit, vegetables and cooked food in local and urban markets (further details here).

The group meets fortnightly in a village church building to save. The share price is K2, so each member may save up to K10 each fortnight. At every second meeting group members can also take out loans and make repayments on existing loans. Members can borrow up to three times the value of their savings.

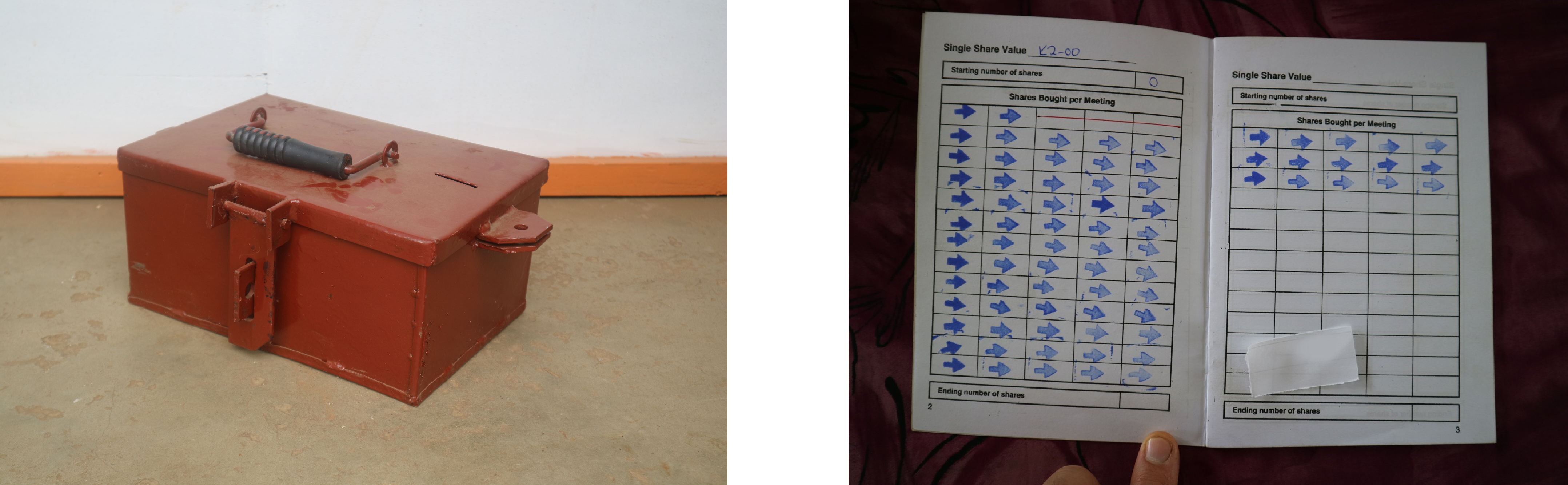

All saving and loan transactions are recorded in the individual passbooks belonging to each member. Share purchases are indicated by stamps to aid those with low literacy levels. The VSLA model has a strong emphasis on transparency, and all transactions are visible to all group members.

Loans may be accessed for the purpose of small-scale business, children’s education, livestock raising and agri-business. Loans must be repaid within three months and a service charge of 30% is charged on the value of the loan. The interest charged is returned to members at the end of cycle share out. The money and passbooks are kept in a heavy steel cash box with three locks, all of which need to be unlocked to open the box. The steel box and each of the three keys to the locks are held by different group members.

Meetings are led by the Chairperson and the management committee. The women’s group is assisted by a local Pastor who is a leading figure within the community, and is the Chairman of the men’s VSLA group.

DATA COLLECTION

Project researchers from Curtin University and the Coffee Industry Corporation have been monitoring and evaluating the effectiveness and success of the scheme. Data has been collected through regular attendance at VSLA group meetings, focus group meetings with men and women and individual interviews with VSLA members. With the permission of the women, data on savings and loans were accessed from their individual passbooks at the end of the first cycle of the VSLA. Basic descriptive statistics were used to summarise the savings and loans data and a preliminary summary report has been completed.

WOMEN’S SAVINGS AND LOANS

Over seven months, the women purchased 1,797 shares (at K2 a share) and invested a total of K3,594. On average, each member bought 75 shares (of a maximum of 80 available to them) worth K150. This was a remarkable achievement for women who prior to the VSLA group had minimal savings.

In total 37 loans were accessed by women during the seven months. All but one woman took out a loan. Of the 37 loans, the large majority were less than K120 and only seven were above K200. Only one woman took out a loan for K300. On average women took out loans smaller than the maximum possible. Over half of the women took out two loans and many women became more confident to take out loans as the cycle progressed.

Only one loan was not repaid by the required repayment date, but was repaid very soon afterwards.

Most women used the loans to seed-fund small economic earning activities. Several used the loans to purchase farm inputs for commercial vegetable production (such as fertiliser, pesticides and seeds) and other women used the loans to start small village retail enterprises selling cooked food or reselling store goods. Profits were used by the women to repay loans, reinvest in the business, diversify into other small income earning activities and to purchase food and clothes for the family. Based on preliminary data analysis the impacts of facilitating access to credit for women have been very positive as women have gained confidence in their ability to move into managing small enterprises and feel a sense of self-pride in their achievements, both individually and as a group.

END OF CYCLE SHARE-OUT

At the end of the savings and loans cycle, the women’s group held their share-out together with the predominantly men’s group. In the women’s group there was a total of K4,640 in the ‘pot’. The total was shared among the 24 women according to the number of shares purchased by each member during the cycle. The share-out occurred in late November and many women allocated their share-out money to school graduation expenses, food for Christmas celebrations and store goods for the household and family members. The share-out was time to celebrate the success and achievements of the VSLA groups.

In February 2019 the women and men’s VSLA groups started a second savings and loan cycle and a new women’s group has been formed at Nagamufa village. Curtin and CIC researchers continue to monitor the progress and impacts of the savings and loans groups on men and women.

References:

CARE International Uganda. (2014). Village Savings and Loans Associations Report Uganda. Retrieved from https://www.care.org.au/wp-content/uploads/2014/12/CARE-VSLA-Report-Uganda-Eco-Devel.pdf

Koczberski, G., Sharp, T., Wesley, J., & Ryan, S. (2019). Identifying Opportunities and Constraints for Rural Women’s Engagement in Small-Scale Agricultural Enterprises in Papua New Guinea. 2018 Village Savings and Loan Associations, Eastern Highlands Province, Papua New Guinea: Preliminary Report. Unpublished report, Curtin University.

Project Title:

Identifying opportunities and constraints for rural women’s engagement in small-scale agricultural enterprises in Papua New Guinea

Project Leader:

Assoc. Prof. Gina Koczberski (Curtin University)

PNG Research Partners:

CARE International Papua New Guinea

Coffee Industry Corporation (CIC)

Other Relevant Publications:

Busse, M. & Sharp, T.L.M. (2019). Marketplaces and Morality in Papua New Guinea: Place, Personhood and Exchange. Oceania 89(2), 126-153.

Sharp, T.L.M. & Busse, M. (2019). Cash crops and markets. In: Hirsch, E., and Rollason, W. (eds) The Melanesian World. Abindon: Routledge, (pp 194-222).

Photo Credits: Dr Tim Sharp and Assoc. Prof. Gina Koczberski